Are you a cat lover who wants to protect your feline friend in the best way possible? Imagine your cat becoming the star of photoshoots, commercials, or even fashion shows.

While that sounds exciting, it also comes with risks that you might not have thought about. That’s where cat modeling insurance comes in. It’s a smart way to keep your pet safe and secure while they shine in front of the camera.

You’ll discover why this type of insurance matters and how it can give you peace of mind every step of the way. Keep reading to find out how to protect your cat’s future in the modeling world.

Benefits Of Cat Modeling

Cat modeling offers many benefits for the insurance industry and policyholders. It helps predict the impact of natural disasters. This leads to better decisions and safer communities. The benefits focus on risk, pricing, and preparedness.

Risk Assessment Accuracy

Cat models use data and science to estimate disaster risks. They analyze weather, geography, and damage history. This creates a clear picture of potential losses. Insurers can spot high-risk areas more precisely. This reduces surprises and unexpected costs. Accurate risk assessment helps protect both insurers and customers.

Improved Insurance Pricing

Better risk data allows fair and balanced pricing. Insurers set premiums that match actual risks. Customers pay reasonable rates based on their location and property. It avoids overcharging low-risk clients and undercharging high-risk ones. Pricing becomes transparent and more competitive. This fairness builds trust and loyalty.

Enhanced Disaster Preparedness

Cat modeling supports planning for future disasters. Governments and businesses use it to prepare resources and responses. It highlights vulnerable areas needing extra attention. Early warnings and readiness reduce damage and loss. Communities become safer and recover faster. Preparedness plans save lives and money.

Types Of Cat Models

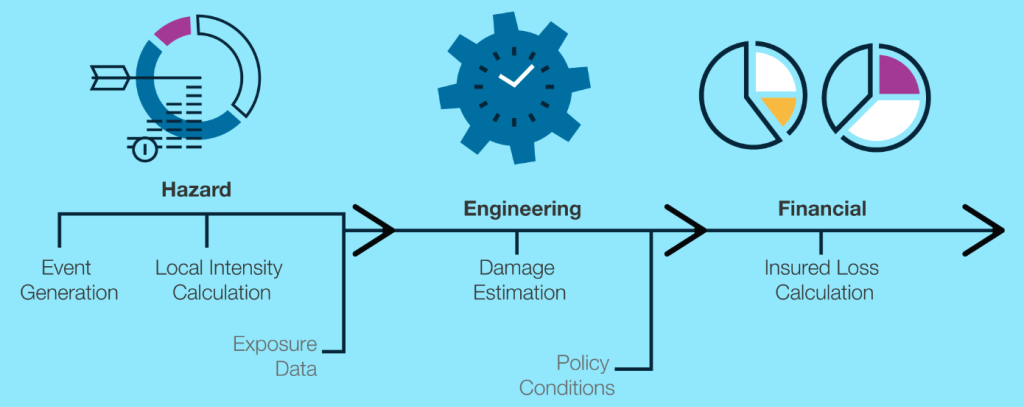

Understanding the different types of catastrophe (cat) models is key to managing your risks effectively. Each model offers unique ways to predict and quantify potential losses from disasters like hurricanes, earthquakes, or floods. Knowing how these models work helps you decide which fits your insurance needs best.

Probabilistic Models

Probabilistic models use statistics to estimate the likelihood and impact of various catastrophic events. They analyze thousands of possible scenarios based on historical data and scientific information. This approach gives you a range of potential losses, helping you prepare for worst-case situations without relying on just one outcome.

For example, a probabilistic hurricane model might simulate hundreds of storms to see how often and how severely they could hit your area. This helps insurers set premiums that reflect real risk levels. Have you ever wondered how insurers decide what coverage to offer after a major disaster? Probabilistic models play a big role.

Deterministic Models

Deterministic models focus on specific, defined events instead of probabilities. They assess the impact of a single, often severe catastrophe scenario to understand potential losses. This method is useful if you want to know your risk exposure from a particular disaster, like a category 5 hurricane hitting your property.

Think about it as running a “what if” test: What if the worst storm hits? How much would you lose? This straightforward approach gives clear answers but doesn’t show the full range of possibilities. Would knowing this worst-case number help you plan your coverage more confidently?

Hybrid Approaches

Hybrid approaches combine elements of both probabilistic and deterministic models to provide a more balanced view. They allow you to see both a range of possible outcomes and specific extreme cases. This mix can give you a deeper understanding of risks and help fine-tune your insurance strategy.

For instance, you might use a probabilistic model to estimate general risk and then apply deterministic tests on critical scenarios. This way, you’re not just guessing the average but also preparing for the worst. Could this dual view improve how you choose your coverage limits?

Data Sources For Cat Modeling

Understanding the data sources behind catastrophe (cat) modeling can significantly enhance your approach to managing risk. These models rely on a rich variety of information to simulate potential losses from natural disasters. Knowing where this data comes from helps you evaluate the reliability and accuracy of the predictions you’re using.

Historical Loss Data

Historical loss data provides a record of past events and their financial impacts. This data helps you identify patterns and frequencies of disasters, which are crucial for estimating future risks.

Insurance companies often maintain extensive databases of claims and damages from previous catastrophes. By analyzing this data, you can see how certain events affected specific regions or property types.

Think about how past hurricanes impacted your area—knowing the magnitude and aftermath can guide your expectations and preparations.

Meteorological Information

Meteorological data includes weather patterns, storm tracks, wind speeds, and rainfall measurements. This information is essential for predicting the likelihood and severity of weather-related disasters.

Satellite imagery and radar data give you real-time updates on developing storms. These tools allow models to simulate the progression of hurricanes, tornadoes, or floods with greater precision.

Have you ever noticed how early warnings from weather services help reduce damage? This shows the power of accurate meteorological data in catastrophe modeling.

Geospatial Data

Geospatial data maps the physical characteristics of locations, such as elevation, land use, and building density. This helps determine how a disaster might spread and which areas are most vulnerable.

Using Geographic Information Systems (GIS), you can layer different data points to see relationships between hazards and populated areas. This visual insight supports better risk assessment.

Imagine knowing exactly which neighborhoods face higher flood risks based on their elevation and proximity to rivers—this knowledge is invaluable for planning and insurance decisions.

Credit: rintupatnaik.medium.com

Challenges In Cat Modeling

Catastrophe modeling plays a vital role in insurance, but it’s not without its hurdles. Understanding these challenges helps you grasp why predictions can sometimes miss the mark. It also shows why continuous improvement is necessary to protect your assets effectively.

Data Quality Issues

Accurate catastrophe models depend heavily on reliable data. Yet, data gaps and inconsistencies often get in the way. You might find missing historical records or outdated information that skew results.

Consider how a small error in earthquake frequency data can change the entire risk assessment. It raises the question: how confident are you in the data feeding your model? Improving data collection and verification processes is essential to reduce these inaccuracies.

Model Uncertainty

No model can perfectly predict the future, and catastrophe models are no exception. Each model makes assumptions and simplifications that add layers of uncertainty. You might see different models giving varied estimates for the same risk.

This uncertainty forces you to think critically about which model fits your needs best. Are you prepared to handle the range of possible outcomes? Testing models under different scenarios can help reveal their strengths and weaknesses.

Changing Climate Patterns

Climate change is shifting the behavior of natural disasters, making past data less reliable. Floods, hurricanes, and wildfires now occur with different intensity and frequency than before. This change challenges your model’s ability to forecast future events accurately.

How often do you update your models to reflect these new patterns? Staying current requires integrating the latest climate science and being ready to adjust your risk strategies. Ignoring these shifts could leave you exposed to unexpected losses.

Role In Insurance Underwriting

Cat modeling plays a crucial role in insurance underwriting. It helps insurers understand the potential impact of natural disasters. This understanding guides decisions about which risks to insure and at what cost. Cat modeling offers data-driven insights that improve risk assessment and financial planning.

Risk Selection

Cat modeling identifies areas with high disaster risk. Insurers use this data to choose which policies to accept. It helps avoid taking on too many risky clients. This careful selection protects the insurer’s financial health.

Policy Pricing

Accurate pricing depends on understanding potential losses. Cat models estimate the damage from events like hurricanes or earthquakes. Insurers set premiums based on these estimates. This ensures fair prices for customers and covers possible claims.

Capital Allocation

Insurers must hold enough capital to pay claims after disasters. Cat modeling predicts the size and frequency of losses. This helps allocate funds efficiently. Proper capital allocation keeps companies stable during big events.

Credit: www.outsource2india.com

Future Trends In Cat Modeling

Understanding the future of catastrophe (cat) modeling is crucial for anyone involved in insurance. As risks evolve, so do the tools used to predict and manage them. Staying ahead means knowing which technologies and approaches will shape the next generation of cat modeling.

Machine Learning Integration

Machine learning is changing how cat models process vast amounts of data. It helps identify patterns that traditional models might miss, improving accuracy in predicting losses.

Imagine your model learning from new events automatically, adjusting predictions without manual updates. This leads to faster responses and more precise risk assessments.

Have you considered how your current cat model adapts to emerging risks? Incorporating machine learning could be a game-changer for your risk management strategy.

Real-time Data Usage

Using real-time data allows cat models to update instantly as new information arrives. This dynamic approach means insurers can react quickly to unfolding events like hurricanes or earthquakes.

With sensors, satellites, and social media feeds, data streams become richer every day. This helps you get a clearer picture of risk as it happens, not just from past events.

What if you could adjust your policies or reserves during a disaster, rather than waiting for the event to conclude? Real-time data makes that possible.

Enhanced Scenario Analysis

Future cat models will offer more detailed scenario analysis, letting you explore a wider range of possible outcomes. This means understanding not just the most likely losses but also rare, extreme events.

By simulating different scenarios, you can test how resilient your portfolio is under stress. This prepares you for surprises and helps in making better business decisions.

Are you confident your current models show the full spectrum of risk your business faces? Enhanced scenario analysis can reveal hidden vulnerabilities before they become costly problems.

Impact On Policyholders

Cat modeling insurance impacts policyholders in several important ways. It helps manage risks linked to natural disasters like hurricanes and earthquakes. This kind of insurance offers more predictable coverage, improving financial security for those living in vulnerable areas. Understanding these effects can guide better choices for protection.

Premium Stability

Cat modeling insurance helps keep premiums steady over time. Insurers use advanced models to predict disaster risks more accurately. This means fewer surprises in premium costs for policyholders. Stable premiums make budgeting easier for families and businesses. It reduces sudden spikes after a major event.

Claims Processing

Claims processing becomes faster and more efficient with cat modeling. Models help insurers estimate damage quickly and fairly. Policyholders receive payouts sooner, which helps in recovery. Clear data reduces disputes over claim amounts. It also lowers paperwork and speeds up decisions.

Risk Mitigation Incentives

Cat modeling encourages policyholders to reduce risks at their properties. Insurers may offer discounts for stronger buildings or flood barriers. This motivates safer construction and better preparedness. Policyholders benefit from lower premiums and less damage. Such incentives create safer communities overall.

Credit: www.insuranceinsider.com

Frequently Asked Questions

What Is Cat Modeling Insurance?

Cat modeling insurance protects insurers from losses due to natural disasters. It uses computer models to estimate potential damages. This helps set premiums and reserves accurately. Insurers can better manage risks linked to catastrophic events.

How Does Cat Modeling Insurance Work?

It uses simulation software to predict disaster impacts on insured properties. Models analyze hazard, exposure, and vulnerability data. Insurers assess potential losses and adjust coverage accordingly. This process improves risk evaluation and pricing strategies.

Why Is Cat Modeling Important For Insurers?

Cat modeling helps insurers anticipate disaster losses more precisely. It reduces uncertainty and financial surprises. Accurate models support better decision-making and risk management. This leads to stable premiums and stronger solvency positions.

Which Disasters Does Cat Modeling Insurance Cover?

Commonly, it covers hurricanes, earthquakes, floods, and wildfires. Models evaluate event frequency, severity, and property exposure. Coverage depends on insurer policies and regional risks. This ensures relevant protection against major catastrophes.

Conclusion

Cat modeling insurance helps protect your furry friend and your work. It covers accidents, illnesses, and other risks that can happen. This insurance gives peace of mind for pet owners and photographers. Choosing the right plan means fewer worries during shoots.

Every cat model deserves safety and care on set. Consider this insurance to keep your cat happy and safe. Protect your investment with a simple, smart choice today.